Turns out Peter Bofinger is not the only German economist who can see MMT across the sea. There is at least one other. Maybe more to follow?

“Say it quietly, but Germany has learnt the lessons of Keynes,” argues Thorvaldur Gylfason.

Mind you, he is talking fiscal largesse, not ECB money. In the “we are all Keynesians now” anglosphere, MMT has long trended through political dinner talk into the mainstream’s inbox. Not that arguments have made the academy pay attention to extra curricular voices. It’s events: QE=QED.

Or as Tyler Mordy puts it, “It always takes a trauma to shake up economic thinking.” In this case : 2008. Since then many observers have made out a QE enabled, de facto MMTish reality all over the place. It’ s the orthodoxy-defying monetary-fiscal mishmash unfolding since 2008 that have pushed, pulled and nudged the mainstream out of their Wicksellian comfort zone. As central banker Stephen Grenville has argued,

“MMT views could fill the gap left by the demonstrated failures, or irrelevancy, of the conventional thinking.”

But mainstreamers’ MMTish rethink doesn’t convert them to MMT.

“Federal Reserve chair Jay Powell sums up the mainstream consensus on MMT : it’s ‘just wrong’ ”. (see below for Grenville articles)

For MMTler Bill Mitchell it looks like this:

“One of the interesting elements of this paradigm tension now is watching the ways the mainstream economists seek to defend their reputations while progressively trying to adopt MMT propositions but deny they are doing that.” More Grenville and Mitchell below (2)

Denial of adaptation or not, you can certainly find any number of articles reworking the rector’s classic rebuke: “MMT is both original and correct ; but what is correct is not original, and what is original is not correct.” ( eg W H Buiter , A Kling , J R Hummel )

MMT just wrong? Many are not so sure. Here is Edward Hadas:

“Most economists on both sides of the debate would probably agree that the fundamental argument is about how the money system works. That may sound arcane, but the implications are concrete. In the MMT world, a government that runs very large fiscal deficits is not necessarily a problem. On the contrary, it can be good for the economy. To conventional economists, that is “voodoo” thinking, as former U.S. Treasury Secretary Larry Summers put it.

Those in Kelton’s camp believe that almost any size deficit is fine, as long as the government’s spending benefits the economy. So the Green New Deal includes a massive investment in solar power, for example. The goal is supposed to be important enough as a long-term investment in the greater good, economically and otherwise, to be worth diverting resources from other uses.

Aside from other objections, traditionalists see such huge government outlays as requiring unsustainable amounts of debt. That’s the main criticism Federal Reserve Chairman Jay Powell was willing to make about MMT in recent congressional testimony. But for the theory’s backers, borrowing is optional. Governments can simply create money directly. This isn’t unheard of, and in some cases it’s no longer even very controversial. It’s what central banks did to fund their purportedly economy-boosting programs of bond buying after the financial crisis a decade ago. …

MMT deserves a serious hearing rather than knee-jerk rejection. Its attention to politics, a deep distrust of debt and the unwillingness to ascribe a quasi-magical motivating power to interest rates all speak in its favour.

Besides, if conventional monetary wisdom is jettisoned, it will not be the first time. From the gold standard to Keynesian fine-tuning, accepted truths have been replaced by something new and different. The current model does not look anything like the last word. MMT is an attractive starting place for a new approach.” read whole article here

MMT right or wrong isn’t really “mein Bier”. There isn’t enough money, politics or globe (yet) in MMT to be a candidate for the next macro paradigm. For sure, if I was a student I’d rather be reading largely relevant Mitchell than 97% irrelevant Mankiw . At least MMT is not DSGE and gives money some credit.

Meanwhile it is almost consoling to watch the mainstream wean itself off its creditless dogma. Here is The Economist sharing the post 2008 learning curve on “the money system” :

“A side-effect of QE is that it leaves the central bank unable to raise interest rates without paying interest on the enormous quantity of electronic money that banks have parked with it. The more money it prints to buy government bonds, the more cash will be deposited with it. If short-term rates rise, so will the central bank’s “interest on reserves” bill. In other words, a central bank creating money to finance stimulus is, in economic terms, doing something surprisingly similar to a government issuing floating-rate debt. And central banks are, ultimately, part of the government.” read whole article here

“Surprisingly similar?” Hmm, sounds a lot like the similarity that got Wray and Mosler going? All based not just on Keynes but What Is Money? By A. Mitchell Innes From The Banking Law Journal, May 1913.

The mainstream rethink may even include a re-discovery of the Ur-Keynesian realisation that it’s not deposits creating loans but the other way round: the “savings glut” is a credit glut ! The Economist again:

“… a number of economists, including Michael Kumhof of the Bank of England, Phurichai Rungcharoenkitkul of the Bank for International Settlements (BIS) and Andrej Sokol of the European Central Bank, take strong issue with it. Echoing work by Claudio Borio and Piti Disyatat of the BIS, they call for a careful distinction between flows of saving and flows of finance. The two are not the same. They need not even move together. The implication is that Mr Bernanke may have got things the wrong way around.”

Note Kumhof etal are central bankers. That’s why The Economist is paying attention.

“For many people (including some economists), it is natural to think that saving must precede investment and that deposits must precede bank lending. It is therefore tempting to see saving as a source of funding and the prime mover in many macroeconomic developments. Mr Kumhof and his co-authors see things differently, giving banks a more active, autonomous role. They give less credit to saving and more to credit.” read the whole article here or below (3)

The Economist concludes here with a bit of dis-embedded fuzziness rather than contextualise Kumhof etal in a manner that would require mentioning Post-Keynesian non-mainstreamers like Steve Keen who did predict the 2008 crash. Not by “…constantly predicting disaster, as Krugman claimed … – but by focusing on the role of debt, finance, and the banking system.” (David Orrell, Quantum Economics Kindle Ed, 4302)

/cdn.vox-cdn.com/uploads/chorus_image/image/63566871/lead.0.jpg?w=863&ssl=1)

As Peter Bofinger writes in “Best of Mankiw: Errors and Tangles in the World’s Best-Selling Economics Textbooks”:

“Mankiw is not alone in thinking that banks are mere intermediaries between savers and investors. It is an expression of the aforementioned real exchange economy modeling of the financial system in (neo)classical theory. It is until today the paradigm which shapes most academic work on financial system issues. Since in the real exchange economy model there is only the aforementioned all purpose good, which becomes available to the financial market only through households’ foregone consumption, the role of banks is reduced to that of a mere conduit between savers and investors. This has nothing to do with reality.”

Reality can be challenging, especially for equilibrium economics. Not least because money only figures as the neutral numeraire. The dominant theory of banking is a gilded anachronism. IS-LM is one of those abstract-into-vacuity formulas that tend to wilt with exposure to reality but nonetheless survive, not least to teach students how to model traffic noise and talk to each other. see critical finance article on LS-IS below (1)

Polemics aside, it struck me how all the MMT/mainstream debates end with their bottom lines firmly pointing to politics. Indeed, what could be more political than the potential, probable, nay inevitable budgetary profligacy of a government able to use direct financing?

exogenous bottom line

endogenous segments of profligacy

But the debate stays typically one-sided. What about the “credit” profligacy of the banks who happen to be the issuers and allocators of up to 97% of M1+M2?

As Martin Wolf argued when temporarily lending his gravitas to MMTish Positive Money , the history of bank and other private “lending” since the off-gold 1970’s reads like unhinged profligacy greedily winding its way toward 2008.

And anyway, if you can’t trust government, why not issue directly to citizens?

They can’t be profligate. They are homo economicus!

Just follow the money…

(1) for updated MMT/QE/Monetary/Fiscal articles etc go to gaiamoneys MMT page(updated 27/1/2021)

GaiaMoney’s MMT page for more links, articles and updates

yahoo finance 5/2/2021 Bank of England boss: ‘No merit’ to claims we’re financing government

/cloudfront-eu-central-1.images.arcpublishing.com/prisa/R4YMH6BNIRFLLBO6ICXFA3SNJQ.jpg?w=863&ssl=1)

elpais.com 25 01 2021 nostalgia-in-economic Strict monetary and fiscal rules do not work at times of economic shock or drastic structural changes by ÁNGEL UBIDE

fxstreet.com 23 01 2021 ECB’s Olli Rehn-calls-yield-curve-control-nonsensical-for-euro-area “ECB is actively managing Eurozone bond yields, but doesn’t call it curve control” Dhwani Mehta

“This new series of OMFIF Insights explores the relationships between monetary and fiscal policy for the world’s major central banks, such as with interest on reserves and the central bank balance sheet. … Bank of England officials may have been surprised when they noticed their asset purchases almost matched state borrowing in 2020. …” read more

ft.com/Jan 2021 “Investors sceptical over Bank of England’s QE programme – FT survey finds big players in bond market think plan is attempt to finance government deficit – In particular, most said they thought the scale of BoE bond buying in the current crisis had been calibrated to absorb the flood of extra bonds sold this year, suggesting they believe the central bank is financing the government’s borrowing.”

“How I Learned to Stop Worrying and Love the National Debt” A Conversation with former Deputy treasury secretary Frank Newman This event will explore common misconceptions regarding the nature of the national debt and its function in the broader context of contemporary U.S. macroeconomic policy. Questions to be addressed include:

What is the national debt comprised of? Why is the national debt different from a personal debt? How accurate are the assumptions behind popular fears over the sustainability of the national debt? How can an accurate understanding of the nature and operations of money inform current debates over the national debt?

Frank Newman works as the Vice-Chairman of Asia for Global Strategic Associates, and has published two books: Six Myths that Hold Back America: And What America Can Learn from the Growth of China’s Economy (2011), and Freedom from National Debt (2012).

www.dw.com mmt-government-spending-debt-and-inflation

“Modern Monetary Theory: Cash-strapped governments a thing of the past?

States with a currency of their own can never run out of money. That’s a core thesis of the Modern Monetary Theory which spilled over to Europe from the US. German economist Dirk Ehnts elaborates on what it’s all about.

en.irefeurope.org New-rules-encourage-EU-governments-profligacy

mining.com Closing the gold window opened the door to Modern Monetary Theory (MMT) Frank Holmes

THE BAR IS FINALLY OPEN by TYLER MORDY (excerpts)

“What exactly is … MMT and why is it getting so much attention? In the last few decades, monetary policy has been widely seen as the most effective tool for managing the economy. However, this assumption is now being called into question. Enter… MMT, a new way of thinking about government spending. Crucially, its swelling supporters argue that fiscal policy should be the primary tool for macroeconomic growth and stability. Whether investors agree with MMT or not is irrelevant. The world is steadily moving toward the adoption of its ideas. …

It always takes a trauma to shake up economic thinking. The Great Depression set policy on a far different path, ushering in a Keynesian era where governments used budgets to fine-tune growth and inflation. That orthodoxy came crashing down in the raging inflation of the 1970s.

From there, central bankers emerged as the leading macroeconomic managers. Of course, interest rates were their weapon of choice. Fed Chairman Paul Volcker, with his towering presence and cigar-smoking press conferences, oversaw a boost in borrowing costs to 20 percent in the 1980s. The cult of the central banker was born.

Alan Greenspan, who led the Fed from 1987 – 2006, took it to a whole new level. Dubbed the “maestro”, he developed an impenetrable linguistic style, clearly indulging — even enjoying — his oracular aloofness. At one point, Greenspan could have stuck a licked finger in the air to convince the public of the economy’s direction.

Monetary policymakers were more like modern-day rock stars. And for good reason. They had routed the inflation enemy. In the US, inflation averaged around 5 percent through the 1970s. Then, it steadily melted. In other developed nations, it has been broadly a similar story.

Central bankers were not shy about celebrating their victory. In the mid-2000s, they would boast of having achieved a “great moderation”: economic and inflation variability had been tamed. Few disagreed that monetary policy was the most effective tool for managing the economy.

Yet all that changed after 2008’s global financial crisis. To fight the downturn, central banks pursued unbridled monetary expansion. Over USD $16 trillion was added to their collective balance sheets. Plenty of voices warned that inflation would come roaring back. It didn’t. Today’s levels of inflation are still lower than a decade ago.

In fact, central bankers have consistently fell short of their inflation and growth targets. The President of the European Central Bank put it plainly in 2014: “deflation is the ogre that now must be fought decisively”.

All of which brings us to today. Globally, almost USD $12 trillion in monetary and fiscal support has been pumped into the economy to fight the impact of Covid-19, leading to soaring budget deficits and public sector debt in all major economies. Have governments done too much? Apparently not. The world has been stuck with inflation stubbornly below official targets and bond yields at new lows.

With this backdrop, it is no surprise that a global policy debate has been sparked. Why does recent experience seem to totally refute standard macroeconomic theory? And what, pray tell, is the right policy mix for the times?

Enter Modern Monetary Theory (MMT), a new way of thinking that has electrified the policy atmosphere …”

read whole article at Ask Forstrong

theconversation.com John Whittaker MMT the-rise-of-economists-who-say-huge-government-debt-is-not-a-problem

socialeurope.eu Germany bows to Keynes, again – Thorvaldur Gylfason

“History is repeating itself. With brute force, the pandemic has brought home a basic economic law: Ivan’s expenditure is Olga’s income. As incomes have collapsed, unemployment has risen (Table 1). In Germany, as well as in France and Italy, the increase in unemployment has been modest, while in the US the unemployment rate has more than doubled—doubling too in my native Iceland. … To finance the stimulus, the German government would borrow nearly €300 billion, equivalent to close to 10 per cent of German gross domestic product and €3,600 per capita. Keynes would have been impressed.”

In their article: “Mainstream Macroeconomics and Modern Monetary Theory: What Really Divides Them?” Arjun Jayadev and J. W. Mason conclude that the

“… feasibility of a functional finance rule for public budgets (is the) central question.”

“We have two concluding thoughts. In our view, it is a mistake for those on the mainstream side of the debate to dismiss MMT supporters as radicals or holders of outré beliefs. They should recognize that MMT is making unconventional policy arguments in a framework of conventional economic analysis. Moreover, the experience of the last decade during which higher levels of debt did not lead to runaway inflation or other obvious costs, and during which conventional monetary policy failed to quickly and reliably close output gaps, should make policy-oriented macroeconomists open to revising their views on the merits of the conventional instrument assignment.

For MMT by contrast, the challenge is to clarify the conditions that make it reasonable to expect a government unconcerned with financial constraints will consistently pursue a fiscal balance consistent with a zero output gap. In order to persuade people in the policy mainstream, MMT must address the real source of their objections, which is, we believe, found not in finance but in political economy. What reason do we have to believe that an elected government that is free to set the budget balance at whatever level is consistent with price stability and full employment would actually do so? This is where the real resistance lies.” Arjun Jayadev and J. W. Mason

Matt Bruenig of Peoples Policy Project seems to agree with Jayadev and Mason and concludes : “If the point of MMT is really about how it would be better to have the fiscal authority manage the price level and the monetary authority manage the debt level — as I thought it might be in 2013 and as Jayadev and Mason argue it is — then you would expect to see a lot more discussion about the competencies and flexibilities of each authority at those tasks. But there is surprisingly little written about such things in these circles.

The real point of MMT seems to be to deploy misleading rhetoric with the goal of deceiving people about the necessity of taxes in a social democratic system. If successful, these word games might loosen up fiscal and monetary policy a bit in the short term. But insofar as getting government spending permanently up to 50 percent of GDP really will require substantially more taxes in the medium and long term, I have to agree with Sawicky and Henwood in saying that MMT seems like a political dead end.” If successful, these word games might loosen up fiscal and monetary policy a bit in the short term. But insofar as getting government spending permanently up to 50 percent of GDP really will require substantially more taxes in the medium and long term, I have to agree with Sawicky and Henwood in saying that MMT seems like a political dead end.”

reddit Bobby Rye Comments on Bruenig/peoples_policy_project_article_on MMT

jacobinmag.com/2019 Modern Monetary Theory Isn’t Helping By Doug Henwood MMT is billed by its advocates as a radical new way to understand money and debt. But it’ll take more than a few keystrokes to change the economy.

economicsfromthetopdown.com/2020 Why Isn’t Modern Monetary Theory Common Knowledge? “I’ve always been baffled why ‘modern monetary theory’ is called a theory. I don’t mean this in a disparaging way. As far as theories of money go, I think modern monetary theory (MMT for short) is the correct one. But having a correct theory of money is a bit like having a correct theory of traffic lights.”

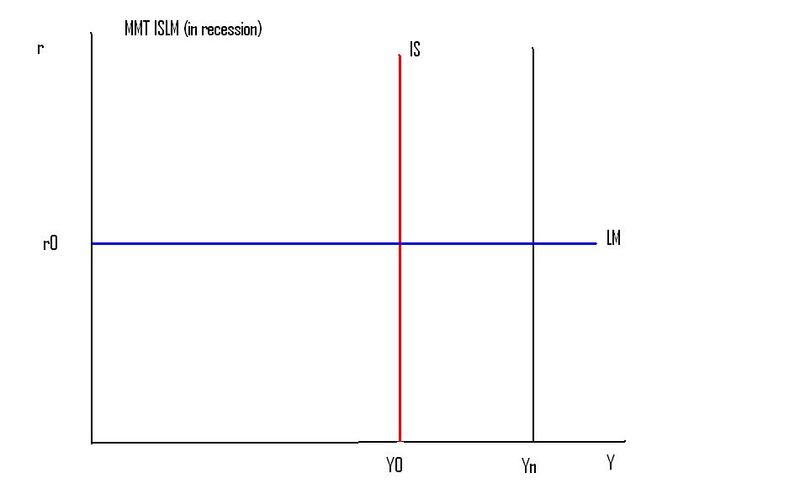

critical finance – KELTON AND KRUGMAN ON IS-LM AND MMT by Jo Michell: “Can this discussion be rescued? Can MMT and IS-LM be reconciled? The answer, I think, turns out to be, “yes, sort of”. I wasn’t the only person pondering this question: several people on Twitter went back to this post by Nick Rowe where he tries to “reverse engineer” MMT using the IS-LM model, and comes up with the following diagram:

Does this help? I think it does. In fact, this is exactly the diagram used by Victoria Chick in 1973, in The Theory of Monetary Policy, to describe what she calls the “extreme Keynesian model” (bottom right):

So how do we use this diagram to resolve the Krugman-Kelton debate? Before answering, it should be noted that MMTers are correct to point out problems with the IS-LM framework. Some are listed in this article by Mario Seccareccia and Marc Lavoie who conclude that IS-LM should be rejected, but “if one were to hold one’s nose,” the “least worst” configuration is what Chick calls the “extreme Keynesian” version.” read the whole article by Jo Michell here

A Simple Post-Keynesian Alternative to IS-LM 2013 ANDREW LAINTON

“Although the Hicksian IS-LM (investment saving–liquidity preference money supply) approach to understanding Keynes (Keynes 1936) (from Hick’s famous 1937 article Mr Keynes and the Classics (Hicks 1937)) has come under severe criticism, not least from Chick above and Hicks (the model’s inventor) himself in 1981 (Hicks 1980-1981). (Pasinetti 1974) lays the blame on the IS-LM for the divergence of orthodox “Keynesian” macroeconomics from the economics of the General Theory. For Joan Robinson IS-LM is was “bastard Keynesianism” for Chick it shows ‘Pseudo dynamics’.”

economicsnetwork.ac.uk Maurice Starkey Credit Creation Theory of Banking

“Bank deposits account for approximately 97% of the money supply in the United Kingdom economy. Bank deposits are sometimes referred to as ‘credit money’ …

…

Whilst most textbooks discuss the money multiplier theory of credit creation, there is limited consideration within academic textbooks of the credit creation theory of banking. However, the Bank of England recently issued a paper which recognises the credit creation theory of banking as a useful theory for understanding the process of money creation (McLeay, Radia, & Thomas, 2014).

Credit creation theory of banking proposes that individual banks can create money, and banks do not solely lend out deposits that have been provided to the bank. Instead, the bank creates bank deposits as a consequence of bank lending. Consequently, the amount of money that a bank can create is not constrained by their deposit taking activities, and the act of bank lending creates new purchasing power that did not previously exist. The repayment of existing debt destroys money, as a consequence of reducing bank loans (asset side of balance sheet) and customer deposits (liability side of the bank balance sheet).

A bank’s ability to create new money, which is referred to as ‘credit money’, is a consequence of a range of factors. Firstly, non-cash transactions account for more than 95% of all transactions conducted within the economy, with non-cash transactions being settled through non-cash transfers within the banking system. Banks’ ability to create credit money arises from combining lending and deposit taking activities. Banks act as the ‘accountant of record’ within the financial system, which enables banks to create the fiction that the borrower deposited money at the bank. Members of the public are unable to distinguish between money that a bank has created, and money saved at the bank by depositors.

Banks’ ability to create credit money is also a consequence of being exempt from the ‘client money rules’. Regulations in the form of the client money rules prevent non-bank organisations creating credit money, because non-bank organisations (for example, stockbrokers, solicitors and accountants) are required to keep clients’ money separate from the non-bank organisation’s assets and liabilities on their balance sheet. However, banks’ exemption from the client money rules enable banks to relabel liabilities on their balance sheet at different stages of the process when extending a loan, which enables banks to expand their balance sheets (Werner, 2014). Exemption from the client money rules enables banks to rename their account payable liability as a customer deposit, despite the money not being a consequence of a customer making a deposit. There is no law, statute or banking regulation that allows banks to reclassify their bank liabilities (accounts payable) as a fictitious customer deposit. Consequently, the legality of banks creating credit money is unclear. Banks’ exemption from the client money rules also means that when a customer deposits money at their bank, the customer no longer owns the money and becomes a general creditor of the bank.” read whole article here

springer.com Keynes’ theory of money and his attack on the classical model L. E. Johnson, Robert Ley & Thomas Cate

“This paper centers on Keynes’ theory of money and his attack on the classical model. Keynes criticized the self-correcting model of the British orthodoxy along two separate lines. In the first, in which Keynes’ theory of money was crucial, he took the institutional variables as given and examined the functional relationships. Keynes’ burden was to undermine what he termed the “classical dichotomy,” where money was a veil, playing no role in determining output and employment. Two key features of the orthodox model were loanable funds and quantity theories, and Keynes’ theory of money emerged from the rejection of these theories. The key to his attack on the classical dichotomy was the speculative demand for money, which he presented as an indirect, unstable function of the interest rate. Hence, Keynes linked money demand to the interest rate. The interest rate was thus determined by monetary variables rather than real factors, contrary to British orthodox opinion. Keynes then demonstrated that intended investment and saving need not be equal at a full employment equilibrium.” read paper here

taxresearch.org Richard Murphy 07/2020 Saturday morning MMT thoughts

for 8 more thoughts in between + interesting comments go here

Summit MMT – Michael Hudson: Finances vs Economy, Credit vs Money

gimms.org/2018/ MMT-and-a-Heterodox-Alternative-Paradigm-Phil-Armstrong.pdf Phil Armstrong

“Orthodox or neo-classical economics failed to predict the global financial crisis (GFC) or even allow for the possibility of such an event occurring. For optimistic heterodox economists the aftermath of the GFC seemed to provide the opportunity to overthrow the hegemonic mainstream paradigm and replace it with a superior alternative; one which provided both better explanations of the operations of a monetary production economy in general and deep insights leading to an understanding of why the GFC might have arisen. However, from the perspective of heterodoxy, this hope proved to be a false dawn; after a brief period of apparent soulsearching, mainstream economists regained their confidence and the paradigm seemed to regain its ascendency, albeit in a slightly modified form. First, this paper examines the methodology employed by mainstream economists and their attitude to academic freedom in order to establish the reasons behind this outcome. Second, it considers the applicability of critical realism both to the study of economics and to the behaviour of the economics

profession itself. Following on from this, the paper goes on to look at the possibility of

constructing a heterodox paradigm, explicitly based upon critical realism, which might have the potential to replace current orthodoxy. The nature of such a paradigm and the potential role for Modern Monetary Theory as a key contributor are evaluated and followed by a consideration of the ways to enhance a new approach’s chances of acceptance.”

GaiaMoney’s MMT page for more links, articles and updates

(2) Grenville + Mitchell

Read Grenville’s 2020 article at source at eurekareport.com or lowyinstitute.org

or read GaiaMoney excerpts below

or read his shorter article from 2019 :

“A consensus has been emerging in America that productivity-enhancing additional expenditure – such as active labour policies and infrastructure – might be undertaken, tentatively exploring the room for deficit expenditures funded by issuing long-term bonds. … But Federal Reserve chair Jay Powell sums up the mainstream consensus on MMT : it’s “just wrong”.

Short excerpt Grenville’s 2020 article:

“Stan Fischer, doyen of mainstream economists, joined the rethink. It was obvious to him (and many others) that monetary policy had lost its power to stimulate the economy. In the post-2008 period, policy interest rates had been lowered to near-zero, and even with real (inflation-adjusted) interest rates clearly negative, entrepreneurs didn’t seize the opportunity of cheap borrowing to expand investment. All that happened was that asset prices were bid up. Fischer saw conventional fiscal policy as ineffective because interest rates would rise to crowd out private expenditure. He advocated ‘helicopter money’ to address the next recession: the central bank should ‘go direct’ in funding what was in effect fiscal policy. Fischer acknowledged that this is a ‘slippery slope’, while asserting that his proposal is quite different from MMT.

But how different is it really? Money-financed deficits are the proposal, and these are to be used when other conventional instruments are ineffective, and when inflation is not a danger. Doesn’t this sound like MMT? In Fischer’s proposal, the threat of uncontrolled fiscal expenditure is prevented by the decision-making being handed over to a central-bank-like independent committee. It is different from MMT because Fischer acknowledges that this is to be used in special circumstances, and there should be an exit strategy. But if conventional macro-policy instruments are not working in the following recession, why not do this again? And in the recession after that? Fischer talks of the importance of an exit strategy, but unless the conventional instruments can be revived, there is no viable exit in sight. …

In the context of this rethink of central bank bond purchases and the role of budget deficits, MMT was well-placed to gain traction: if deficits were effective and central bank bond purchases didn’t cause inflation, MMT views could fill the gap left by the demonstrated failures, or irrelevancy, of the conventional thinking.”

Or read Bill Mitchell’s critique of Grenville: “An old central banker trying to come to terms with MMT – not quite getting there”. Excerpts:

“One of the interesting elements of this paradigm tension now is watching the ways the mainstream economists seek to defend their reputations while progressively trying to adopt MMT propositions but deny they are doing that.”

“So while Stephen Grenville is correct in writing “MMT has revived the old Keynesian message: if the economy has spare capacity, governments should expand the budget to bring the economy back to full employment” it is also true that this ‘old message’ was not abandoned because it was proven to be incorrect or would lead to damaging policies. It was abandoned because shifting the policy focus away from ‘full employment’ and fiscal activism towards ‘full employability’ repressed wages growth, allowed for deregulation to tilt the balance of power in the distributional system towards capital, and facilitated major shifts in national income distribution away from workers. It was a power play not a knowledge revolution.”

Grenville 2020 article long excerpt

MODERN MONETARY THEORY AND MAINSTREAM ECONOMICS CONVERGING

14 JULY 2020 Stephen Grenville gives a detailed account in the Eureka Report on Modern Monetary Theory (MMT), which after a decade on on the periphery of economic discussion, has recently surged in popularity.

GaiaMoney excerpt :

MMT has revived the old Keynesian message: if the economy has spare capacity, governments should expand the budget to bring the economy back to full employment. Certainly, policy measures shouldn’t push this beyond the economy’s productive capacity, or inflation would result. …

“So why isn’t everyone signing up to the MMT message?

‘Follow the money’, the detectives say. For simplicity, let’s assume the deficit expenditure is in cash. This circulates in the economy, stimulating demand and expanding GDP. Some of the cash will remain in the hands of the public in the form of extra currency balances, but most of it will end up in the banking system, as deposits. The banks don’t want to hold zero-interest cash, so they hand it back to the central bank, increasing the banks’ reserves at the central bank.

It is these banks’ reserves that are, in effect, funding the budget deficit. They are NOT free of interest cost, as central banks pay the banks a market-related interest return. And they DO increase official-sector debt – these reserves are a liability of the central bank to the banking system, and so should properly be counted as part of official debt.

In short, the core MMT promise, sometimes implicit, is interest-free financing which doesn’t add to official debt. This is clearly wrong. Milton Friedman got this much right: ‘there is no free lunch’. “

… but there could be with a different banking system? Like one where all citizen’s have a central bank account as well as whatever accounts and use independent payment systems?

“Where does the MMT narrative fit within the development of the mainstream macro-economic thinking? The 2008 global financial crisis was the catalyst in bringing the MMT story towards the mainstream. In 2008 the US Fed began quantitative easing (QE) …

…the first element of the rethink of economics after 2008 was the recognition that central banks could buy government bonds, create base money, interest rates would fall rather than rise and inflation was unaffected.

The second element of the rethink was the role of government deficits. Most countries applied deficit stimulus in 2009, but within a year austerity was imposed through surplus budgets, motivated by concerns about government debt that had built up during the global crisis. With budget surpluses subtracting from demand, the recovery was lacklustre.

By 2013, some macroeconomists (such as Olivier Blanchard, then chief economist at the IMF) were recognizing that the austerity had been more damaging than expected. The Fund had advocated austerity, believing that the budget multiplier was low so the surpluses would not damage the recovery. By 2013, Blanchard recognized the error. The austerity was holding back the recovery.

By 2019 Blanchard went one step further, arguing that, with interest rates well below the rate of nominal GDP growth, governments could afford to run modest deficits without the debt/GDP ratio rising, with a strong implicit recommendation that they should do so. Even the IMF (whose surplus-promoting doctrines were so entrenched that its initials were widely quoted as standing for ‘It’s Mainly Fiscal’) was urging countries with ‘fiscal space’ to run deficits to promote growth.

Donald Trump’s company tax cuts in 2017, ill-conceived as they were, added weight to the evidence that budget deficits worked effectively to affect growth – the US recovery accelerated and unemployment fell to record-low levels. The huge expansion of Fed base money (‘money printing’) had no effect on inflation, and interest rates continued to fall, to historically low levels.

In short, the mainstream view that deficit spending was ineffective was shown to be wrong, at least in the context of an economy working at less than full capacity.

Other mainstream economists joined the re-think of macro-economics. Larry Summers called for substantial government expenditure on infrastructure to address the problem of ‘secular stagnation’ – another old idea revived almost a century after Alvin Hansen had first worried about the economy’s apparent inability to sustain growth.

Adair Turner, who headed the UK Financial Services Authority during the 2008 crisis, was an early (2015) convert to the heretical idea of ‘helicopter money’, essentially the same as MMT. With monetary policy and conventional fiscal policy ineffective, central banks should fund fiscal-policy expansion.

Source: Larry Summers, “Reflections on the new ‘Secular Stagnation hypothesis’”

Stan Fischer, doyen of mainstream economists, joined the rethink. It was obvious to him (and many others) that monetary policy had lost its power to stimulate the economy. In the post-2008 period, policy interest rates had been lowered to near-zero, and even with real (inflation-adjusted) interest rates clearly negative, entrepreneurs didn’t seize the opportunity of cheap borrowing to expand investment. All that happened was that asset prices were bid up. Fischer saw conventional fiscal policy as ineffective because interest rates would rise to crowd out private expenditure. He advocated ‘helicopter money’ to address the next recession: the central bank should ‘go direct’ in funding what was in effect fiscal policy. Fischer acknowledged that this is a ‘slippery slope’, while asserting that his proposal is quite different from MMT.

But how different is it really? Money-financed deficits are the proposal, and these are to be used when other conventional instruments are ineffective, and when inflation is not a danger. Doesn’t this sound like MMT? In Fischer’s proposal, the threat of uncontrolled fiscal expenditure is prevented by the decision-making being handed over to a central-bank-like independent committee. It is different from MMT because Fischer acknowledges that this is to be used in special circumstances, and there should be an exit strategy. But if conventional macro-policy instruments are not working in the following recession, why not do this again? And in the recession after that? Fischer talks of the importance of an exit strategy, but unless the conventional instruments can be revived, there is no viable exit in sight.

In the context of this rethink of central bank bond purchases and the role of budget deficits, MMT was well-placed to gain traction: if deficits were effective and central bank bond purchases didn’t cause inflation, MMT views could fill the gap left by the demonstrated failures, or irrelevancy, of the conventional thinking.

Then came COVID-19 The immediate response in COVID-affected countries was massive budget deficits combined with central bank actions which, whatever their motivation and objective, involved the purchase of large amounts of government bonds which are, de facto, funding the deficits.

Part of the central bank response to COVID has been in the form of QE, but part is in the form of money-financing of the budget deficit. Doesn’t this mean that the MMT strategy has been widely adopted? Far from it, at least according to the mainstream economists. Even those (now quite a few) who advocate policies that look to be close to MMT are adamant that they have not signed up. Why not? What distinctions remain to separate these policies from MMT?

A key issue here is the well-established idea that monetary policy should be clearly separated from fiscal…

Mainstream economists such as Fischer and Turner who advocate money-finance deficits would distinguish their proposals from MMT by asserting that theirs are once-off remedies in response to special circumstances. There would be a clear exit strategy and a time-bound return to a clear distinction between monetary and fiscal policy. MMT proponents see their prescription as being the on-going norm, to be implemented whenever there is unused capacity in the economy.

Post-COVID, this ‘just this one time’ distinction seems naïve. There will be no quick return to budget balance, and the substantial expansion of government debt will be one more factor inhibiting a rise in policy interest rates. …

What, then, are the proper limits, and the true constraints, on money-financed deficits? There are three common concerns:

Inflation risks Friedman’s legacy was a wide-spread and firmly-held belief that if the central bank produced excessive base money, inflation was inevitable. This might have been true when Friedman wrote it. The financial sector was heavily regulated, …

Budget profligacy … Thus it is hard to dismiss MMT simply on the grounds that it would inevitably lead to budget profligacy. Big spending governments would still be constrained by the capacity of the economy to produce without setting off inflation. The danger of MMT is that the implicit promise of free and debt-less expenditure might in practice over-ride this inflation constraint. The independence of the deficit-setting process might be sorely tested.

Financial repression and fiscal dominance Savings and investment decisions, pension management, and financial market calculation of asset prices, all depend critically on the input of a sensible and relevant interest rate. Current interest rates, negative in real (inflation-adjusted) terms, cannot be the long-term equilibrium. This may turn out to be the main down-side not only of MMT, but of the post-2008 central bank policies.

Conclusion

MMT proponents must feel that their moment has arrived at last. The core elements of their proposal are being more widely accepted by mainstream economists and now, with COVID, being put into practice. Big deficits are being rolled out everywhere, partly funded by central bank money creation. Debt hawks and inflation alarmists have largely gone silent, and the bond-market vigilantes are no-where to be seen. The MMT promise of free funding for deficits has turned out to be almost true because interest rates are so low and expected to remain so for the foreseeable future. Their view that inflation is caused by running the economy ‘too hot’, rather than by excessive money creation, is now more widely accepted.

MMT views have fallen on receptive minds in the US political process, as left-of-centre ideas were promoted, particularly by Democratic candidates over the past five years.

These are radical changes in the economic orthodoxy, compared with three decades ago. But strongly entrenched scepticism about the MMT message means that MMT cannot claim victory in the sense of converting mainstream economists to the MMT views. It was events – particularly the 2008 crisis, its limp recovery and the impotence of monetary policy – that caused a rethink of macro-economics among some of the most influential mainstream economists. As the mindset of these conventional economists asymptotes closer to the MMT message, these resisters might revive the old put-down: ‘this MMT proposal is both original and correct; but what is correct is not original, and what is original is not correct.’ But they might have to acknowledge that policy prescriptions have largely converged.

read the whole article at eurekareport.com or lowyinstitute.org

(3) The Economist article 2020

GaiaMoney’s MMT page for more links, articles and updates